Suriname Oil & Gas - structural relationships

Download PDF: Suriname Oil & Gas: structural relationships

Most foreign companies that sign a Production Sharing Contract in Suriname do not sign it from Houston, London or Dubai. They sign it from a Netherlands B.V. The pattern is so consistent that it is worth asking out loud: why do the overwhelming majority of Suriname oil and gas PSCs run through a Dutch holding company, and why does almost every serious international party end up with the same setup?

The short answer is that the structure you put in place before your first contract decides how much tax leaves the country when the profit does. By the time the first barrel is sold, the holding structure is already fixed, and changing it later is expensive or impossible. This article explains how the Surinamese upstream regime, the PSC contractor group and the international holding structure fit together, and why a Netherlands B.V. with a Suriname branch keeps winning the comparison.

What is a Production Sharing Contract in Suriname?

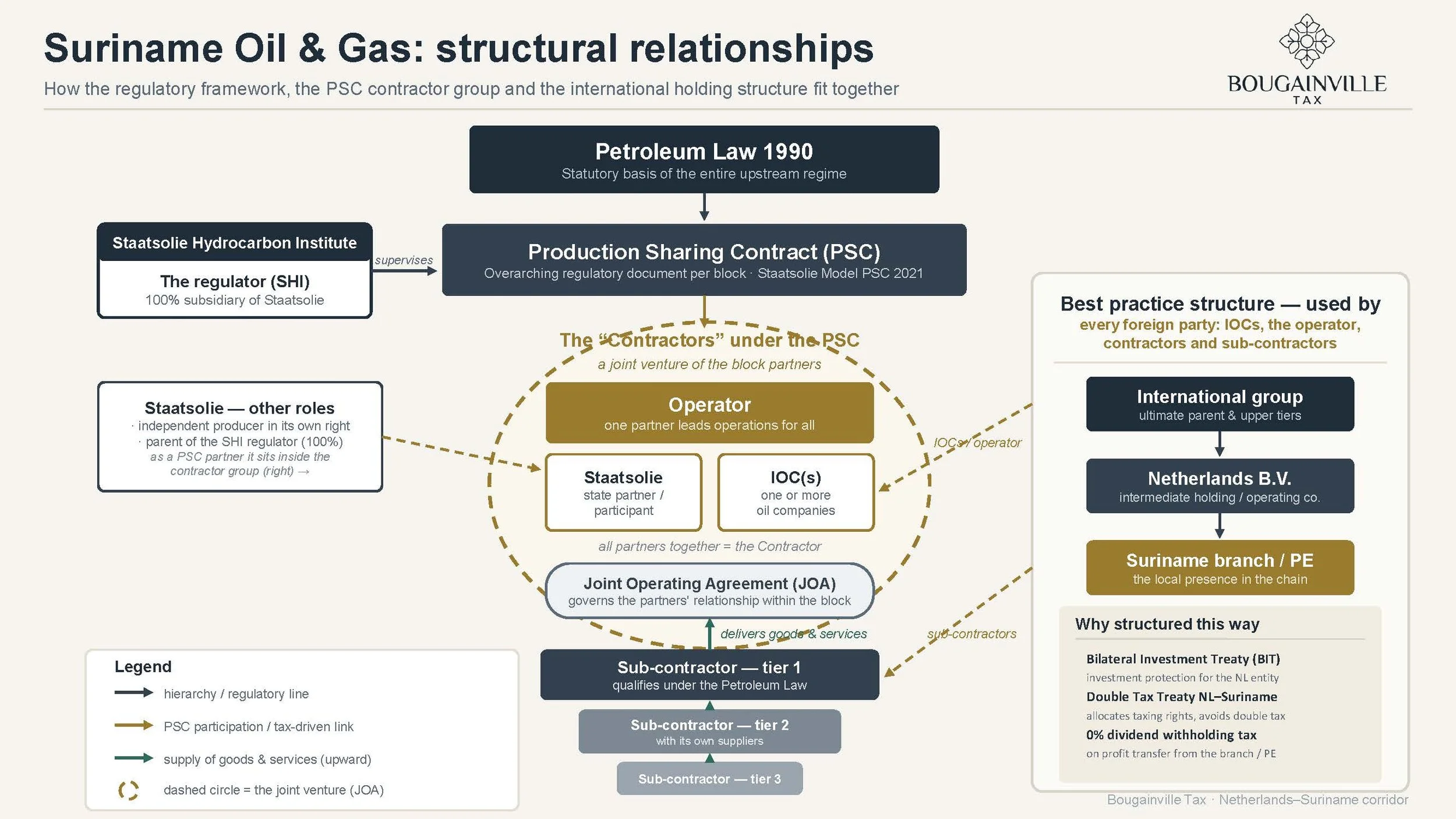

Suriname's upstream petroleum sector rests on the Petroleum Law 1990, the statutory basis of the entire regime. Under that law, the state oil company Staatsolie is authorised to enter into petroleum agreements with qualified international companies. The instrument it uses is the Production Sharing Contract, or PSC, based on Staatsolie's publicly available model PSC. The PSC is the overarching regulatory document for each block: it sets out the work programme, the split of production between the state and the contractor, cost recovery, and the fiscal terms.

Regulation of the industry sits with the Staatsolie Hydrocarbon Institute (SHI), a wholly owned subsidiary of Staatsolie. SHI supervises the PSCs and oversees petroleum operations carried out by international oil companies. Staatsolie therefore wears more than one hat: it is the parent of the regulator, it is a participant in the blocks, and it is an independent producer in its own right.

Who are the "Contractors" under a Suriname PSC?

Under a PSC, the party on the other side of the table from the state is not usually a single company. It is a group. Together, the block partners form what the contract calls the Contractor. That group is a joint venture: one or more international oil companies (IOCs), often Staatsolie itself as a state participant, and an operator, the partner that leads day-to-day operations on behalf of all of them. The relationship between the partners inside the block, how costs and decisions are shared, is governed by a separate Joint Operating Agreement (JOA).

Below the contractor sit the sub-contractors, in tiers. A tier-one sub-contractor qualifies directly under the Petroleum Law; below it are further tiers of suppliers delivering goods and services up the chain. The important point for structuring is that every layer of this chain, the IOCs, the operator, the contractors and the sub-contractors, faces the same question: through which jurisdiction should it hold its Surinamese activity? And almost all of them reach the same conclusion.

Why structure a Suriname oil and gas investment through a Netherlands B.V.?

The best-practice structure used by foreign parties looks like this: an international group at the top, a Netherlands B.V. as the intermediate holding or operating company in the middle, and a Suriname branch or permanent establishment as the local presence in the chain. Three features make the Dutch B.V. the natural choice, and they reinforce each other.

The first is the tax treaty. The Netherlands and Suriname are linked by a bilateral tax arrangement dating back to 1975. It allocates taxing rights between the two countries, sets the conditions under which Suriname may tax the activity of a Dutch enterprise, and provides the mechanism that stops the same profit from being taxed twice. The second is investment protection, which comes from a separate instrument: the 2005 agreement on the encouragement and reciprocal protection of investments between the Kingdom of the Netherlands and the Republic of Suriname, in force since 2006. The third is the way profit leaves the country, which is where the structure earns its reputation.

How is a Suriname branch or permanent establishment taxed?

Oil and gas exploration and exploitation in Suriname create a permanent establishment (PE) by definition. A foreign company that explores or produces is treated as carrying on business through a PE and is taxed in Suriname on the profit attributable to it, at the standard corporate income tax rate of 36 percent. There is no avoiding Surinamese tax on Surinamese upstream profit, nor should there be: that is the price of access to the resource.

The decisive question is what happens when that after-tax profit moves up to the foreign owner. Here the branch or PE structure does something a subsidiary cannot. Suriname does not levy a withholding tax when a branch remits its profit to its foreign head office. Because a branch and its head office are the same legal entity, the remittance is not a dividend, so no dividend withholding tax arises. The rate on the profit that flows from the Suriname PE up to the Netherlands B.V. is, in effect, zero.

A Surinamese subsidiary would behave differently. It would pay a dividend, and that dividend would attract Suriname's domestic dividend withholding tax, reduced under the Netherlands–Suriname tax arrangement but not to zero. The branch or PE route avoids that leakage entirely. And at the Dutch end, the profit of the Suriname permanent establishment is in principle exempt from Dutch corporate income tax under the object exemption for foreign business profits. The result is profit taxed once in Suriname, repatriated without withholding, and not taxed a second time in the Netherlands.

What does the Netherlands–Suriname tax treaty actually do?

A tax treaty is not a discount coupon; it is a rulebook for which country may tax what. The Netherlands–Suriname arrangement determines when Surinamese activity rises to the level of a permanent establishment, how business profits are allocated between the two states, how dividends, interest and royalties are treated, and how each country relieves double taxation on income the other has already taxed. For a long-life, capital-intensive upstream investment, that certainty is worth more than a headline rate. It tells investors, financiers and partners in advance how the cash will be taxed across its whole life, which is exactly what a project-finance lender and a board want to see before they commit.

What investment protection does the Netherlands–Suriname BIT provide?

Tax efficiency means little if the underlying investment is not safe. The 2005 bilateral investment treaty between the Netherlands and Suriname gives a Dutch entity fair and equitable treatment, protection against unlawful expropriation, the free transfer of capital and returns, and access to international arbitration if a dispute with the state arises. Upstream petroleum is a multi-decade, sunk-cost commitment in a single jurisdiction; the ability to invoke treaty protection, and to enforce it outside the local courts, is part of what makes the Dutch entity bankable. This is protection that an offshore shell in a jurisdiction without such a treaty simply does not have.

Why not a UAE, BVI or similar company?

On a slide, a company in the United Arab Emirates, the British Virgin Islands or a comparable jurisdiction looks cheaper and simpler. It rarely survives contact with the real decision criteria. There is no tax treaty between Suriname and those jurisdictions to allocate taxing rights or to cap withholding on outbound flows. There is no investment treaty to protect the investment against state action. The economic substance needed to defend the structure against anti-abuse rules, both Surinamese and international, is usually absent, which puts the intended treatment at risk. The permanent-establishment profit-allocation position is weaker, because there is no treaty framework to anchor it. And in an industry under intense scrutiny from banks, partners and regulators, an offshore holding company attracts financing, banking and reputational friction that a Dutch B.V. does not. Once the treaty network, the investment protection, the absence of withholding on branch remittances and the profit-allocation discussion are all on the table, the apparent saving disappears.

What is the PE profit allocation discussion, and why does it matter?

The structure does not run itself, and one technical exercise matters more than any other: deciding how much profit belongs to the Suriname permanent establishment and how much remains with the Netherlands B.V. This is also where the tax treaty does its quietest but most important work. Surinamese domestic law casts a wide net over the sector, treating, in principle, all oil and gas related profit as Surinamese and taxable in Suriname. Left to that domestic rule alone, a foreign investor is caught in full, with little room to argue that part of the value was created elsewhere. The Netherlands–Suriname tax treaty replaces that domestic trap with a principled allocation. Under the authorised OECD approach, the PE is treated as if it were a separate, independent enterprise, and profit is attributed according to the functions performed, the assets used and the risks assumed in each location, supported by transfer-pricing analysis and documentation. Allocate too little to Suriname and you invite a local assessment you cannot defend; allocate too much and you lose the benefit of the structure and risk double taxation. This is where good structuring earns its keep, and where a generic offshore setup, with no treaty to fall back on, stays caught in the domestic net.

Reading the diagram

The diagram below brings the whole picture onto one page. On the left and in the centre sits the Surinamese regulatory world: the Petroleum Law 1990 at the top, the PSC beneath it, SHI as the regulator, and the contractor group, the operator, Staatsolie and the IOCs, inside the dashed circle of the joint venture, with the sub-contractor tiers feeding goods and services upward. On the right sits the international holding structure that every foreign party builds against it: the international group at the top, the Netherlands B.V. in the middle, and the Suriname branch or PE on the ground, with the three reasons it is built this way set out underneath, the investment treaty, the tax treaty, and the absence of withholding on the profit transfer.

Get the structure right before the first contract

The reason 90 percent of Suriname's PSCs run through a Dutch B.V. is not fashion. It is the sum of a working tax treaty, a real investment treaty, a permanent-establishment route that repatriates profit without withholding, a domestic object exemption that prevents a second layer of tax, and a profit-allocation framework you can actually defend. Each of these can be undone by a structure chosen for the wrong reasons, and almost none of them can be retrofitted after the contract is signed. The time to design the holding structure is before the first PSC is on the table, not after the first assessment lands.

Frequently asked questions

Why is a Dutch B.V. used for Suriname oil and gas? Because the Netherlands has both a tax treaty and an investment treaty with Suriname, a domestic object exemption for foreign permanent-establishment profit, and a structure, the Suriname branch or PE, that lets profit be repatriated without withholding tax. Together these give certainty on taxation, protection of the investment, and efficient repatriation that low-tax offshore jurisdictions cannot match.

Does Suriname tax the profit a branch sends to its head office? No withholding tax is imposed when a branch remits profit to its foreign head office. A branch and its head office are the same legal entity, so the transfer is not a dividend and no dividend withholding tax applies. A Surinamese subsidiary paying a dividend would be treated differently.

What is the corporate income tax rate in Suriname? The standard corporate income tax rate is 36 percent, and it applies to the profit of a permanent establishment of a foreign company, including upstream oil and gas operations.

Is there a tax treaty between the Netherlands and Suriname? Yes. The two countries are linked by a bilateral tax arrangement dating back to 1975 that allocates taxing rights, defines when a permanent establishment exists, and relieves double taxation.

Is the investment protected by treaty? Yes. The 2005 bilateral investment treaty between the Netherlands and Suriname, in force since 2006, provides fair and equitable treatment, protection against unlawful expropriation, free transfer of returns and access to international arbitration.

Can a UAE or BVI company be used instead? It can, but it usually should not. Those jurisdictions have no tax treaty and no investment treaty with Suriname, typically lack the substance to defend the structure against anti-abuse rules, and leave the permanent-establishment profit-allocation position weaker, on top of banking and reputational friction.

This article is general information on the structuring of oil and gas investments in the Netherlands–Suriname corridor and is not tax or legal advice. The right structure depends on the specific facts of your project. Figures and rates reflect the position at the time of writing and can change.